The basics of finance and financial literacy: Assets & Liabilities

Almost everyone aspires to improve their financial situation. But very few take the time to become financially literate by understanding the key concepts for long-term wealth building.

Some individuals accumulate wealth due to a strong understanding of financial principles. This often involves building up resources that can increase in value over time (assets). Others may focus more on consumption rather than the accumulation of income-generating assets (liabilities).

Some individuals accumulate wealth due to a strong understanding of financial principles. This often involves building up resources that can increase in value over time (assets). Others may focus more on consumption rather than the accumulation of income-generating assets (liabilities).

QUOTE

The truth is that money does not make you rich; knowledge does.

Big ideas

- Wealth can be an important factor in building financial literacy. This includes knowing the difference between assets and liabilities and reinvesting income.

- One approach to financial security involves understanding cash flow – how money is earned and spent – and identifying ways to use surplus income in a sustainable way. Exchanging time directly for income often has limitations, so alternative approaches to managing money may be worth exploring.

- A lack of understanding about financial terms like assets and liabilities can lead to missed opportunities for long-term financial growth.

What is financial literacy?

Financial literacy is a term used to denote an understanding of key financial concepts, such as assets, liabilities, diversification, time value of money, risk vs reward, and other terms.

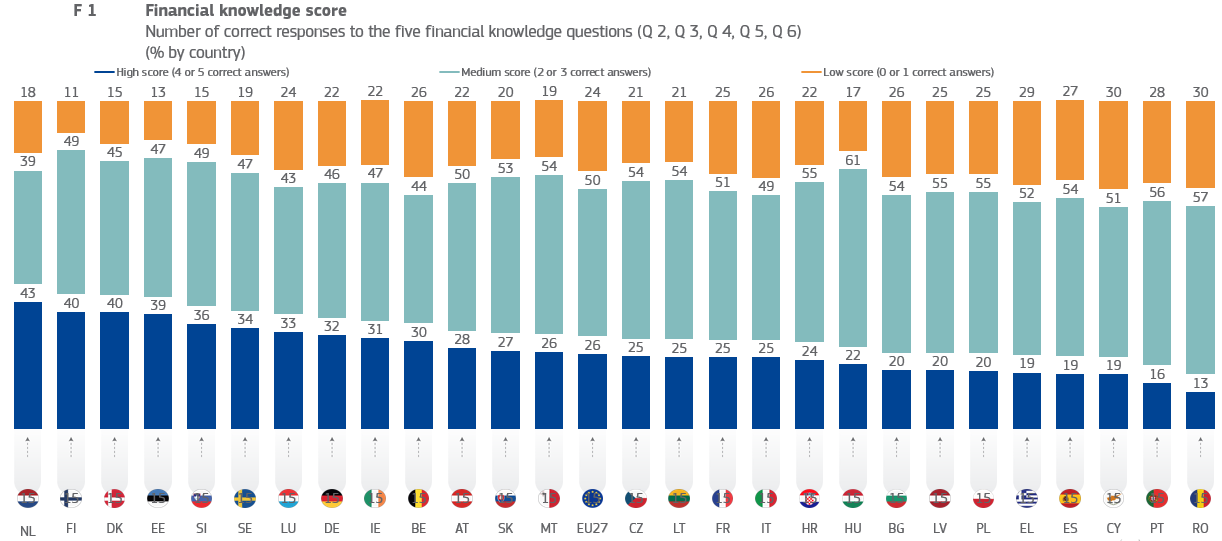

Financial literacy across the EU in 2023 remains modest, with only 18% of citizens demonstrating a high level of financial understanding, while another 18% score low. The best-performing countries include the Netherlands, Denmark, Finland, and Estonia. While most Europeans grasp the concept of inflation, only 45% understand compound interest, and just 20% know how interest rates impact bond prices. Financial behaviours are more positive, with 90% of respondents saying they consider affordability before purchases and track expenses. Comfort with digital financial services is high (77%), but trust in investment advice remains low, at only 38%. Financial resilience also varies – only one-third of EU citizens could cover six months of expenses without income, and 16% have no emergency savings. Most do not feel confident about their retirement finances, highlighting a strong need for improved financial education across demographics.

Economic challenges such as inflation, rising living costs, and broader financial policies can often lead to frustration. However, research suggests that improving financial literacy can help individuals feel more equipped to manage the ups and downs of the market. For example, understanding how various savings options work may help lessen the effects of inflation, depending on the wider economic context.

Historically, some people have built wealth during economic downturns. While circumstances certainly play a role, many financial educators emphasise the value of a strong mindset and long-term planning. Making informed choices, particularly during periods of market uncertainty, can be an important aspect of building financial resilience.

Economic challenges such as inflation, rising living costs, and broader financial policies can often lead to frustration. However, research suggests that improving financial literacy can help individuals feel more equipped to manage the ups and downs of the market. For example, understanding how various savings options work may help lessen the effects of inflation, depending on the wider economic context.

Historically, some people have built wealth during economic downturns. While circumstances certainly play a role, many financial educators emphasise the value of a strong mindset and long-term planning. Making informed choices, particularly during periods of market uncertainty, can be an important aspect of building financial resilience.

The so-called Kiyosaki quadrant

In terms of financial literacy, Robert Kiyosaki defines people into four groups:

- Employee

- Self-employed

- Business owner

- Investor

The Business Owner and Investor groups are differentiated from the other two groups, on the basis that their income was derived from assets/employees, and they did not trade time for money.

For both employees and the self-employed, the majority of income tends to go towards covering day-to-day living expenses. Like employees, self-employed individuals often find it difficult to delegate tasks, which can place a natural cap on their earning potential. While this is one viewpoint, it is important to consider a range of financial strategies and assess what best suits your personal circumstances.

Robert Kiyosaki emphasises the importance of distinguishing between assets and liabilities. If something does not generate positive cash flow, it cannot be considered a true asset. His message is not about getting rich quickly, but rather about prioritising the acquisition of income-generating assets over liabilities and building long-term financial stability.

Individuals at the lower end of the socio-economic scale often own few, if any, assets and tend to accumulate liabilities – sometimes without recognising the difference. There are also blurred lines. A car, for example, is often thought of as an asset, but in many cases, it depreciates in value and incurs ongoing costs such as insurance, fuel, maintenance, and registration. In this sense, it does not generate income and instead requires regular expenditure, making it more of a liability than an asset.

Robert Kiyosaki emphasises the importance of distinguishing between assets and liabilities. If something does not generate positive cash flow, it cannot be considered a true asset. His message is not about getting rich quickly, but rather about prioritising the acquisition of income-generating assets over liabilities and building long-term financial stability.

Individuals at the lower end of the socio-economic scale often own few, if any, assets and tend to accumulate liabilities – sometimes without recognising the difference. There are also blurred lines. A car, for example, is often thought of as an asset, but in many cases, it depreciates in value and incurs ongoing costs such as insurance, fuel, maintenance, and registration. In this sense, it does not generate income and instead requires regular expenditure, making it more of a liability than an asset.

Why the quadrant matters

The general idea suggests that building wealth often involves finding ways for money to generate additional income over time, rather than relying solely on earned income from work.

When income arrives in a bank account, it can be reinvested into some kind of asset that bears fruits, without additional labour. However, this requires careful consideration of individual risk tolerance, time, and goals.

Building long-term financial stability can be difficult when relying only on active income, which refers to money earned directly through work, as this approach has its limitations. Over time, it may lead to increased pressure and strain on personal well-being. An alternative some individuals explore is developing systems, such as businesses, that can generate income without requiring constant direct involvement.

Along with this, Kiyosaki also stresses the importance of understanding key financial concepts like knowing how to read cash flow statements, income statements, and balance sheets. Learning how to interpret these can help individuals better understand their own finances or evaluate financial decisions more clearly.

When income arrives in a bank account, it can be reinvested into some kind of asset that bears fruits, without additional labour. However, this requires careful consideration of individual risk tolerance, time, and goals.

Building long-term financial stability can be difficult when relying only on active income, which refers to money earned directly through work, as this approach has its limitations. Over time, it may lead to increased pressure and strain on personal well-being. An alternative some individuals explore is developing systems, such as businesses, that can generate income without requiring constant direct involvement.

Along with this, Kiyosaki also stresses the importance of understanding key financial concepts like knowing how to read cash flow statements, income statements, and balance sheets. Learning how to interpret these can help individuals better understand their own finances or evaluate financial decisions more clearly.

Understanding financial statements

For investors and business professionals, decoding the common financial statements is essential. There are many nuances to financial statements and many ways to make the numbers tell a different story.

So be sure to understand what the numbers really represent. It is also useful to be mindful of certain quirks that are industry-specific.

So be sure to understand what the numbers really represent. It is also useful to be mindful of certain quirks that are industry-specific.

With this in mind, the three most important statements include the:

- Cash flow statement – tracks actual cash inflows and outflows over a period. It consists of operating, investing, and financing activities. Operating cash flow shows core business earnings, investing covers asset purchases or sales, and financing reflects borrowing or dividends.

- Income statement, aka Profit & Loss or P&L – reports a company’s revenue, expenses, and net income over a specific period. It starts with total sales, deducts costs and operating expenses, and ends with net profit or loss. This statement helps investors assess profitability.

- Balance sheet – provides a snapshot of a company’s financial position at a given date. It lists assets, liabilities, and shareholder equity. Assets include cash, receivables, and equipment. Liabilities cover debts and obligations. Equity represents retained earnings and investments.

Assets vs liabilities

Assets and liabilities apply to individuals just as they do to businesses.

DEFINITION OF ASSETS

Assets are anything a person owns that has value and can generate future benefits.

This includes cash, savings accounts, stocks, bonds, real estate, vehicles, and personal belongings like jewelry.

Assets can be liquid (easily converted to cash, like a checking account) or illiquid (harder to sell quickly, like property or retirement accounts). The more assets a person has, the stronger their financial position.

This includes cash, savings accounts, stocks, bonds, real estate, vehicles, and personal belongings like jewelry.

Assets can be liquid (easily converted to cash, like a checking account) or illiquid (harder to sell quickly, like property or retirement accounts). The more assets a person has, the stronger their financial position.

DEFINITION OF LIABILITIES

Liabilities are financial obligations or debts that an individual owes.

These include mortgages, car loans, student loans, credit card debt, and personal loans.

Liabilities are categorised as short-term (due within a year) or long-term (spanning years, like a home loan or student debt).

These include mortgages, car loans, student loans, credit card debt, and personal loans.

Liabilities are categorised as short-term (due within a year) or long-term (spanning years, like a home loan or student debt).

EXAMPLE

Imagine a person who owns a home worth £300,000 (an asset) but has a £200,000 mortgage (a liability).

Their net worth is £100,000 (assets minus liabilities).

If they also have £10,000 in savings and £5,000 in credit card debt, their total assets rise to £310,000, while total liabilities increase to £205,000, making their net worth £105,000.

The goal in financial planning is often to improve this net position by managing debt and increasing savings or other resources.

Their net worth is £100,000 (assets minus liabilities).

If they also have £10,000 in savings and £5,000 in credit card debt, their total assets rise to £310,000, while total liabilities increase to £205,000, making their net worth £105,000.

The goal in financial planning is often to improve this net position by managing debt and increasing savings or other resources.

What are the basic concepts of finance?

Some of the most essential concepts involved in financial literacy are cash flow, time value of money, risk vs reward, market efficiency, and financial leverage.

- Cash flow – measures the actual movement of money in and out of a business over a period. Positive cash flow means a company can cover expenses and invest in growth, while negative cash flow may indicate financial strain or investment in future expansion.

- Time value of money (TVM) – the principle that money today is worth more than the same amount in the future due to earning potential. It explains why interest rates exist and why investors prefer immediate returns. Future cash flows are discounted to show their present value, helping in valuation decisions.

- Risk and return – the relationship between potential rewards and the uncertainty of achieving them. Higher returns usually require taking on more risk, while lower risk investments offer steadier but smaller gains. Investors look at risk through volatility, economic conditions, and company performance to balance risk and reward.

- Market efficiency – financial markets show all available information, meaning assets are fairly priced. In efficient markets, it is difficult to consistently achieve above-average returns without taking on extra risk.

- Financial leverage – the use of borrowed money to increase potential returns. While leverage can amplify gains, it also raises financial risk. Companies and investors must balance debt with the ability to manage repayment and interest costs.

Why financial literacy is important

Financial literacy is relevant for everyone, not just finance professionals. Having a basic understanding of how to budget, manage expenses, and make informed financial choices can lead to more stability and better decision-making.

QUOTE

Formal education will make you a living; self-education will make you a fortune.

Some have contended that money should be taught to teenagers in schools, stressing the importance of the subject. Ultimately, anyone who is financially illiterate should learn to speak the language and use money wisely. Otherwise, financial difficulties are not only likely, but inevitable.

Financial illiteracy could result in home foreclosure or extensive debt, and an inability to pay for black swan events like sudden medical emergencies or natural disasters. Certain individuals could also be more at risk of financial scams, for lack of monetary awareness.

Financial illiteracy could result in home foreclosure or extensive debt, and an inability to pay for black swan events like sudden medical emergencies or natural disasters. Certain individuals could also be more at risk of financial scams, for lack of monetary awareness.

Key component | Description |

Budgeting and expense management | Creating and maintaining a plan to allocate income across essential expenses, discretionary spending, and savings goals. Helps avoid overspending and builds financial discipline. |

Saving and investing | Setting aside money regularly for future needs (e.g. emergencies or major purchases) and using investment vehicles (like stocks or funds) to potentially grow wealth over time. |

Debt management | Understanding different types of debt (credit cards, loans, mortgages), knowing how interest works, and applying strategies to reduce and manage debt effectively. |

Retirement planning | Making informed decisions to secure income for later life, including pensions, private retirement accounts, and investment planning tailored to long-term goals. |

Insurance and risk management | Using insurance (health, life, property, etc.) to protect against unexpected financial losses, and understanding how to balance risk vs. reward in personal finance. |

Understanding financial products | Gaining knowledge of key financial concepts such as inflation, compound interest, savings accounts, credit, and more complex tools like bonds and derivatives. |

Financial literacy covers a wide range of areas, including budgeting, managing debt, understanding credit scores and interest rates, the importance of diversification, and developing a habit of saving. It also involves navigating a broad variety of investment products and making informed choices about them.

A common principle in personal finance is the idea of paying yourself first, which involves prioritising contributions to assets such as stocks, bonds, real estate, or commodities when managing income. Some people choose to use that money to build savings or explore different financial options, depending on their needs.

A common principle in personal finance is the idea of paying yourself first, which involves prioritising contributions to assets such as stocks, bonds, real estate, or commodities when managing income. Some people choose to use that money to build savings or explore different financial options, depending on their needs.

Recap

The principles of financial literacy can be more impactful than the possession of money alone, as demonstrated by the fact that some lottery winners face financial hardship despite sudden wealth.

Achieving financial stability often requires informed decisions around saving, budgeting, and understanding how various financial resources work. While outcomes depend on individual choices and circumstances, applying money strategically, supported by strong financial education, can help with long-term planning.

While financial understanding is important, market and life events also influence financial outcomes. Many well-known investors suggest that reading widely and gaining a strong understanding of financial markets can be helpful. However, any investment decision should be made with careful consideration of one’s individual financial goals, risk tolerance, and personal circumstances.

One way to reflect on financial habits is to consider how much of your income typically goes toward assets that have the potential to generate returns, compared to spending on liabilities that may reduce overall wealth. This assessment can quickly tell you which part of the quadrant that you belong to.

Achieving financial stability often requires informed decisions around saving, budgeting, and understanding how various financial resources work. While outcomes depend on individual choices and circumstances, applying money strategically, supported by strong financial education, can help with long-term planning.

While financial understanding is important, market and life events also influence financial outcomes. Many well-known investors suggest that reading widely and gaining a strong understanding of financial markets can be helpful. However, any investment decision should be made with careful consideration of one’s individual financial goals, risk tolerance, and personal circumstances.

One way to reflect on financial habits is to consider how much of your income typically goes toward assets that have the potential to generate returns, compared to spending on liabilities that may reduce overall wealth. This assessment can quickly tell you which part of the quadrant that you belong to.

FAQ

Q: What is meant by financial liquidity?

Financial liquidity refers to how quickly and easily assets can be converted into cash without losing value. High liquidity means assets, like cash or stocks, can be quickly accessed. Low liquidity means assets, such as real estate or collectibles, may take longer to sell and could be sold at a loss if urgent.

Q: What are the 5 major asset classes?

The 5 major asset classess are:

1. Cash

2. Real estate

3. Stocks

4. Bonds

5. Personal property.

Cash is generally considered highly liquid. Real estate, stocks, and bonds are commonly known for having different characteristics in terms of liquidity, risk, and market accessibility. Personal property such as vehicles and jewellery may hold value, though their liquidity can vary depending on market conditions.

1. Cash

2. Real estate

3. Stocks

4. Bonds

5. Personal property.

Cash is generally considered highly liquid. Real estate, stocks, and bonds are commonly known for having different characteristics in terms of liquidity, risk, and market accessibility. Personal property such as vehicles and jewellery may hold value, though their liquidity can vary depending on market conditions.

Q: What are the 5 types of liabilities?

The 5 types of liabilities include:

1. Current liabilities

2. Long-term liabilities

3. Secured liabilities

4. Unsecured liabilities

5. Contingent liabilities

Current liabilities are short-term debts due within a year, while long-term liabilities extend beyond one year. Secured liabilities are backed by assets, while unsecured liabilities are not. Contingent liabilities depend on future events or conditions.

1. Current liabilities

2. Long-term liabilities

3. Secured liabilities

4. Unsecured liabilities

5. Contingent liabilities

Current liabilities are short-term debts due within a year, while long-term liabilities extend beyond one year. Secured liabilities are backed by assets, while unsecured liabilities are not. Contingent liabilities depend on future events or conditions.

Q: What are some general principles of personal finance?

Educational frameworks often include:

1. Save regularly

2. Make informed decisions about financial tools

3. Diversify your resources

4. Manage debt prudently

5. Plan for long-term goals

1. Save regularly

2. Make informed decisions about financial tools

3. Diversify your resources

4. Manage debt prudently

5. Plan for long-term goals

Q: Is financial literacy important?

Yes, financial literacy is essential, as it enables individuals to make informed decisions about budgeting, saving, investing, and managing debt. With rising living costs, increasing financial responsibilities, and changes in retirement planning, a solid understanding of personal finance supports long-term financial stability and independence.

Q: When is a good time to start saving for retirement?

Many educational sources recommend starting early, as it allows time for savings to potentially grow. However, this depends on individual circumstances and goals.

This information is not investment advice. Do your own research.