The pros and cons of investing in mutual funds

If you are on the lookout for a hands-off, stable, long-term, highly diversified financial solution and don't mind paying a little extra, then mutual funds might be the answer.

The mutual fund market is huge, largely because they are a default investment for many pension plans. The term mutual fund is more of a US thing but keep reading to learn the equivalent terms used in the UK and Europe.

The mutual fund market is huge, largely because they are a default investment for many pension plans. The term mutual fund is more of a US thing but keep reading to learn the equivalent terms used in the UK and Europe.

QUOTE

Many financial innovations, such as the increased availability of low-cost mutual funds, have improved opportunities for households to participate in asset markets and diversify their holdings.

– Janet Yellen (former Fed Chair and US Treasury Secretary)

– Janet Yellen (former Fed Chair and US Treasury Secretary)

Big ideas

- Mutual funds offer access to a large variety of securities, such as stocks, bonds, money market instruments, across sectors. This is done by pooling investor money to be managed by an experienced professional.

- The benefits of mutual funds include diversification, management, and low investment minimums. However, fees and expenses have to be watched since they tend to be higher than investing in passively managed index funds.

- Unlike other financial products, mutual funds are priced once a day. Pricing is based on the Net Asset Value (NAV), a core feature in mutual funds.

What is a mutual fund?

DEFINITION

A mutual fund is a professionally managed investment programme funded by shareholders that trades in diversified holdings.

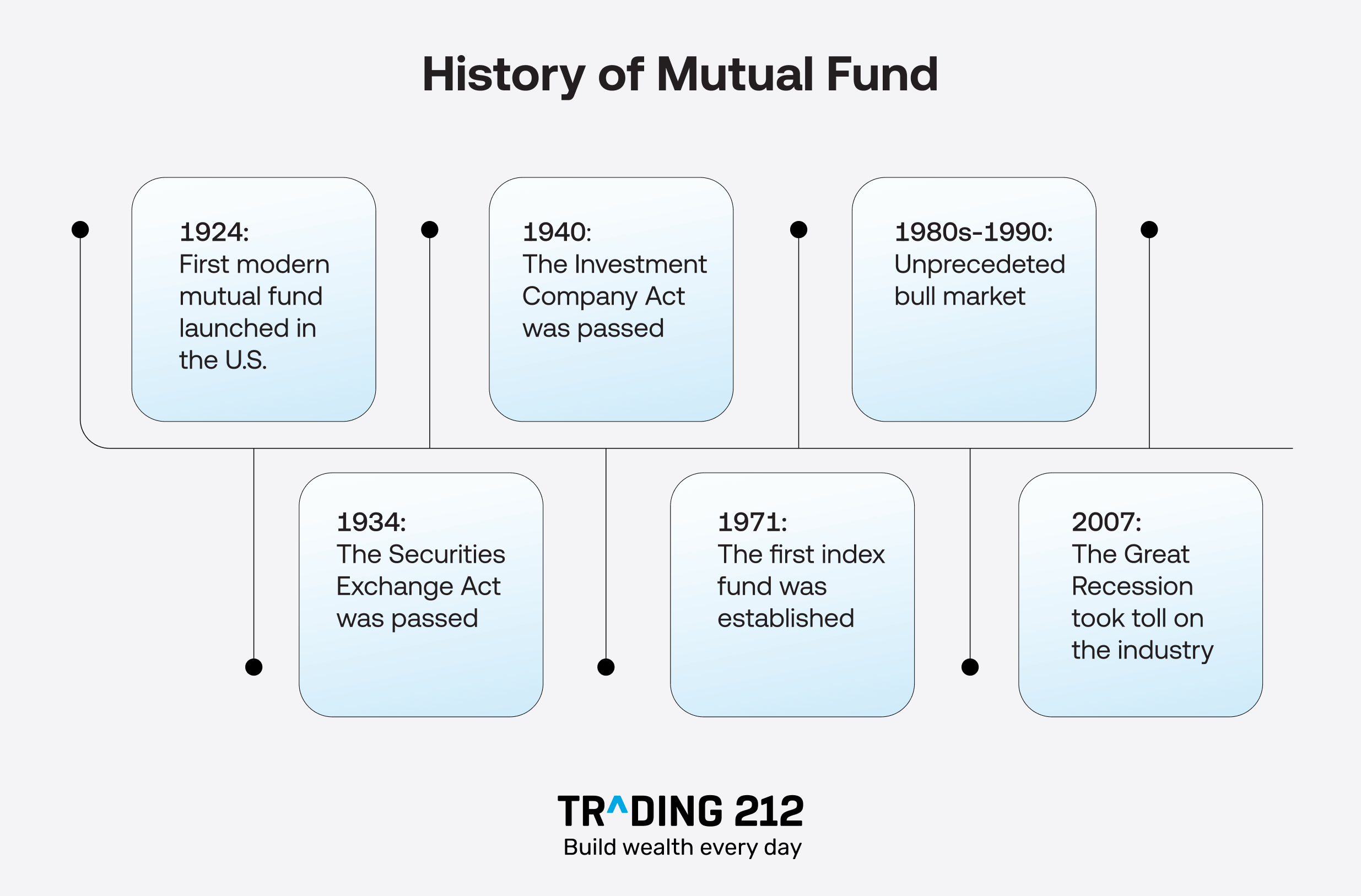

The oldest modern mutual fund was launched in the US in 1924. However, it was not until the 1980s that they really became a staple of Western investment, due to major bull runs in the same decade. The ETF, a recent variant of the mutual fund that trades like a stock, popularised the vehicle further.

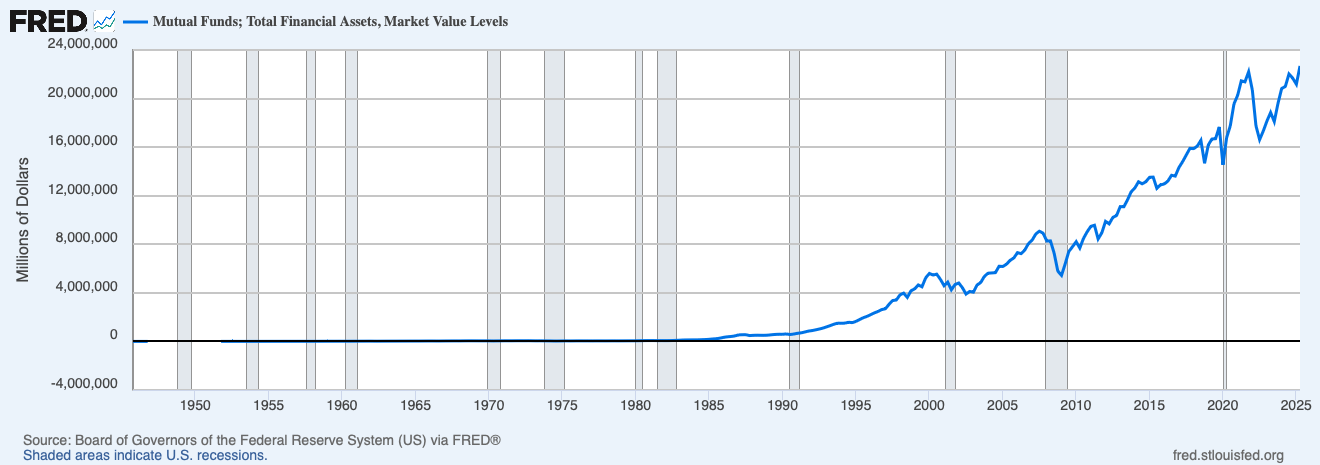

US households account for the vast majority of all mutual fund assets. Funds are spread across different securities, offering the benefit of diversification. This is why they are a default option for people preparing for retirement, where risk reduction is the number one concern.

How a mutual fund works

A mutual fund collects money from many investors and uses it to buy a group of assets, usually stocks, bonds, or both. The fund is managed by a team that follows a specific investment objective. The investment objective is explained in the fund’s prospectus, which also includes fees, risks, and holdings.

The idea is simple. By investing in a mutual fund, you become a shareholder of the fund itself. You don’t own the underlying securities directly – you own units of the fund. For example, if a mutual fund has a total NAV of £1,000,000 and 10,000 units in circulation, the NAV per unit would be £100. Owning two units would therefore represent an investment worth £200.

You can also invest steady amounts per month as opposed to buying whole units. A pension plan holder might invest £200 each month into a mutual fund over the course of many decades. The plan holder will not be looking to take profits or cut losses on a daily basis with NAV price movements. Returns accrue over time. It is also easy to switch between funds.

Mutual funds are regulated by the SEC in the US, the FCA in the UK, and ESMA in the EU. They must follow rules on transparency, pricing, and reporting. Most funds also disclose their full portfolio regularly.

The idea is simple. By investing in a mutual fund, you become a shareholder of the fund itself. You don’t own the underlying securities directly – you own units of the fund. For example, if a mutual fund has a total NAV of £1,000,000 and 10,000 units in circulation, the NAV per unit would be £100. Owning two units would therefore represent an investment worth £200.

You can also invest steady amounts per month as opposed to buying whole units. A pension plan holder might invest £200 each month into a mutual fund over the course of many decades. The plan holder will not be looking to take profits or cut losses on a daily basis with NAV price movements. Returns accrue over time. It is also easy to switch between funds.

Mutual funds are regulated by the SEC in the US, the FCA in the UK, and ESMA in the EU. They must follow rules on transparency, pricing, and reporting. Most funds also disclose their full portfolio regularly.

Mutual funds in the UK, Europe, and the US

In the US, mutual funds are mainly open-ended and regulated by the SEC. They price once per day after the markets close. Investors buy or sell shares directly from the fund at the NAV. Many US funds are actively managed, though index funds are also common.

Source: US Federal Reserve of St. Louis

Source: US Federal Reserve of St. LouisIn the UK, the main types are unit trusts and OEICs. Unit trusts use a trust structure and issue units. OEICs are corporate structures that issue shares. Both are open-ended and priced daily. They are regulated by the FCA. UK funds often focus on income or growth and may have different share classes.

Feature | UCITS | OEICS | Mutual Funds |

Full name | Undertakings for Collective Investment in Transferable Securities | Open-Ended Investment Company | Mutual fund |

Region | Europe | UK | US |

Rules and safety | Very strong EU rules to protect investors | UK rules, often also follow EU-style rules | Follows US laws from the SEC |

Price changes | Price goes up or down based on the total value of the fund | Price goes up or down based on how the fund’s investments are doing | Price goes up or down based on value of what the fund owns |

Currency | Usually Euro (€), sometimes other currencies | Usually British Pounds (£) | Usually US Dollars ($) |

Pros | Well-regulated and transparent | Flexible and safe (following UCITS rules) | Huge range of options |

Cons | Hard to understand, high fees for foreign investors | Mainly for UK investors | Hard to buy outside the US, tax rules might not suit everyone |

In Europe, UCITS funds dominate. These follow EU rules and can be sold across borders. UCITS are widely used by retail and institutional investors. They are open-ended, highly regulated, and often priced daily. Each region has small structural and regulatory differences, but all aim to pool money and invest in a mix of assets.

Types of mutual funds with examples

Mutual funds fall into four basic types:

- Equity

- Fixed income

- Balanced

- Money market

Equity funds invest mainly in stocks. They aim for growth. These funds can focus on certain sectors, regions, or styles (like value or growth). Returns depend on the stock market.

EXAMPLE

An example of an equity OEIC in the UK is the Invesco UK Equity Fund. As of the latest data in 2025, the NAV is approximately £2.37. The fund has assets under management (AUM) of around £1.2 billion. The yield is about 2.4%.

The main fees for this fund are the expense ratio (2.47%), the initial charge (3%), with a maximum annual charge of 2%. There is no exit charge, meaning funds can be sold without fees.

This fund focuses on investing primarily in UK companies, aiming for capital growth by selecting stocks with strong growth potential. The fund manager uses a bottom-up approach.

Past performance is no guarantee of future results. This information is not investment advice. Do your own research. The calculations are hypothetical and intended solely for educational use.

The main fees for this fund are the expense ratio (2.47%), the initial charge (3%), with a maximum annual charge of 2%. There is no exit charge, meaning funds can be sold without fees.

This fund focuses on investing primarily in UK companies, aiming for capital growth by selecting stocks with strong growth potential. The fund manager uses a bottom-up approach.

Past performance is no guarantee of future results. This information is not investment advice. Do your own research. The calculations are hypothetical and intended solely for educational use.

Fixed income funds put money into bonds and other debt. These funds try to provide regular income, usually with lower price swings than equity funds. They are generally considered lower risk, though not risk-free.

Balanced funds mix stocks and bonds in one fund. The mix can vary depending on the fund's goal. Some lean more toward growth, others toward income. The fund prospectus will have all the information needed to understand whether it is suitable for your needs or not.

Balanced funds mix stocks and bonds in one fund. The mix can vary depending on the fund's goal. Some lean more toward growth, others toward income. The fund prospectus will have all the information needed to understand whether it is suitable for your needs or not.

EXAMPLE

The Fidelity Multi Asset Income Fund is an example of a balanced OEIC in the UK. As of the latest data in 2025, the NAV is approximately £1.48.

The fund has assets under management of around £3.6 billion. The yield is approximately 4.5%, reflecting its focus on making income through a mix of equity and fixed-income investments.

The main fees for this fund are the expense ratio (0.8%) with a transaction cost of 0.23%. The maximum annual charge is 0.5% with no entry or exit fees.

The fund aims to deliver a blend of income and moderate capital growth by investing in a diversified range of asset classes, including stocks, bonds, and alt investments.

Past performance is no guarantee of future results. This information is not investment advice. Do your own research. The calculations are hypothetical and intended solely for educational use.

The fund has assets under management of around £3.6 billion. The yield is approximately 4.5%, reflecting its focus on making income through a mix of equity and fixed-income investments.

The main fees for this fund are the expense ratio (0.8%) with a transaction cost of 0.23%. The maximum annual charge is 0.5% with no entry or exit fees.

The fund aims to deliver a blend of income and moderate capital growth by investing in a diversified range of asset classes, including stocks, bonds, and alt investments.

Past performance is no guarantee of future results. This information is not investment advice. Do your own research. The calculations are hypothetical and intended solely for educational use.

Money market funds (MMF) invest in short-term debt, such as Treasury bills and commercial paper. They aim to keep the price stable while giving modest returns. This is one of the safest options on the market.

Mutual fund categories

While there are four major types of mutual funds, there are many more variants and subcategories. The different variants are outlined in the table below.

Mutual fund type | Description | Pros | Cons |

Equity | Invest mainly in company stocks. | Higher return potential. Good for long-term growth. | More price swings. Sensitive to market moves. |

Bond | Invest in government or corporate debt. | Regular income. Usually less volatile than stocks. | Interest rate risk. Lower growth over time. |

Index | Track a specific market index like the S&P 500. | Low fees. Broad market exposure. | No manager decisions. Follows the index exactly. |

Multi asset | Combine stocks, bonds, and other assets. | Built-in diversification. Balanced risk. | Less control over asset mix. Can be complex. |

Money market | Invest in short-term debt like T-bills or cash. | Very stable. Easy to access. | Low returns. Can lag inflation. |

Income | Focus on assets that pay dividends or interest. | Steady payouts. Can support income needs. | Limited growth. Can be sensitive to rate changes. |

Target date | Adjust mix of assets based on a future date (like a retirement year). | Hands-off. Shifts automatically over time. | Less flexible. Allocation may not fit every investor. |

Balanced | Hold a fixed ratio of stocks and bonds. | Simple way to stay diversified. | No customisation. Allocation may not suit every market cycle. |

International | Invest in non-domestic companies or markets. | Exposure to global growth. Currency benefits possible. | Currency risk. Foreign markets can behave differently. |

Sector/Theme | Focus on one industry (like tech) or theme (like clean energy). | High potential if the sector does well. | Can be volatile. Less diversified. |

Socially responsible | Choose assets based on ESG criteria (environment, social, governance). | Aligns with values. Gaining popularity. | Limited choices. May miss some profitable sectors. |

Are there drawbacks to mutual funds?

Despite mutual funds being a hugely popular investment option, it is always useful to stand back and see the other side of public opinion. Critics of mutual funds highlight the high fees and lack of flexibility.

QUOTE

Most investors will be better off buying a low-cost index fund.

— Warren Buffett (on mutual fund management fees)

— Warren Buffett (on mutual fund management fees)

Another common criticism is that mutual funds often underperform the market due to these fees and the challenge of consistently picking winning stocks. John Bogle, founder of Vanguard, also criticised actively managed funds, noting that the majority of actively managed funds underperform their benchmarks.

Mutual funds lack the ability to react quickly to market changes since they are constrained by daily trading limits. Investors must wait until the end of the trading day for share price adjustments, missing potential opportunities. Lastly, mutual funds are subject to taxes on capital gains, even if the investor hasn’t sold their shares, which can further reduce overall returns.

Mutual funds lack the ability to react quickly to market changes since they are constrained by daily trading limits. Investors must wait until the end of the trading day for share price adjustments, missing potential opportunities. Lastly, mutual funds are subject to taxes on capital gains, even if the investor hasn’t sold their shares, which can further reduce overall returns.

Recap

In a market full of investment choices, mutual funds remain a structured and widely used option. Still, like any financial product, their value depends on how well they match your personal goals.

This is why the most important item to keep in mind is what your goals are – once you are clear on what you want, there could be thousands of financial products that meet the criteria.

Once you understand an investment in its entirety – taxes, costs, risks, rewards – then you can make a clear decision. After this, it just takes time, patience, and dedication to see results.

This is why the most important item to keep in mind is what your goals are – once you are clear on what you want, there could be thousands of financial products that meet the criteria.

Once you understand an investment in its entirety – taxes, costs, risks, rewards – then you can make a clear decision. After this, it just takes time, patience, and dedication to see results.

FAQ

Q: What are the 4 types of mutual funds?

The four main types of mutual funds are equity funds, fixed-income funds, money market funds, and balanced funds.

Equity funds invest mostly in stocks.

Fixed-income funds focus on bonds.

Money market funds go into short-term debt.

Balanced funds mix stocks and bonds. Each has its own mix of risk and return.

Equity funds invest mostly in stocks.

Fixed-income funds focus on bonds.

Money market funds go into short-term debt.

Balanced funds mix stocks and bonds. Each has its own mix of risk and return.

Q: How do mutual funds work?

A mutual fund pools money from many people. A fund manager then uses that money to buy stocks, bonds, or other assets. You buy shares in the fund. If the value of the fund’s investments goes up, your shares go up in value. You can also earn from dividends or interest.

Q: What is the equivalent of mutual funds in the UK?

In the UK, mutual funds are called unit trusts and open-ended investment companies. Both pool money from many investors and spread it across many holdings. They are managed by fund managers. The structure and rules are slightly different, but the main idea is the same as mutual funds.

Q: Are mutual funds safe?

Mutual funds carry different levels of risk depending on what they invest in. Money market funds tend to be more stable. Equity funds can move up and down more. The fund’s performance depends on the market and the choices made by the manager. Prices can go down as well as up.

Q: Is an ETF a mutual fund?

An ETF is a type of mutual fund, but it trades on a stock exchange like a share. Most ETFs track an index. Mutual funds are priced once a day. ETFs move during the trading day. They are usually cheaper to run. Both spread your money across many investments.

Q: What is the difference between open-ended and closed-end funds?

Open-ended funds issue and redeem shares at the NAV, based on investor demand. Their share supply is not fixed. Closed-end funds, on the other hand, issue a fixed number of shares in an initial offering, and shares are traded on an exchange like stocks. Their price can differ from the NAV based on market demand.