Compound interest: The eighth wonder of the world

Few methods of building wealth offer taking relatively low risk with proven results over time. Compound interest is one of them, allegedly described by Albert Einstein as the eighth wonder of the world.

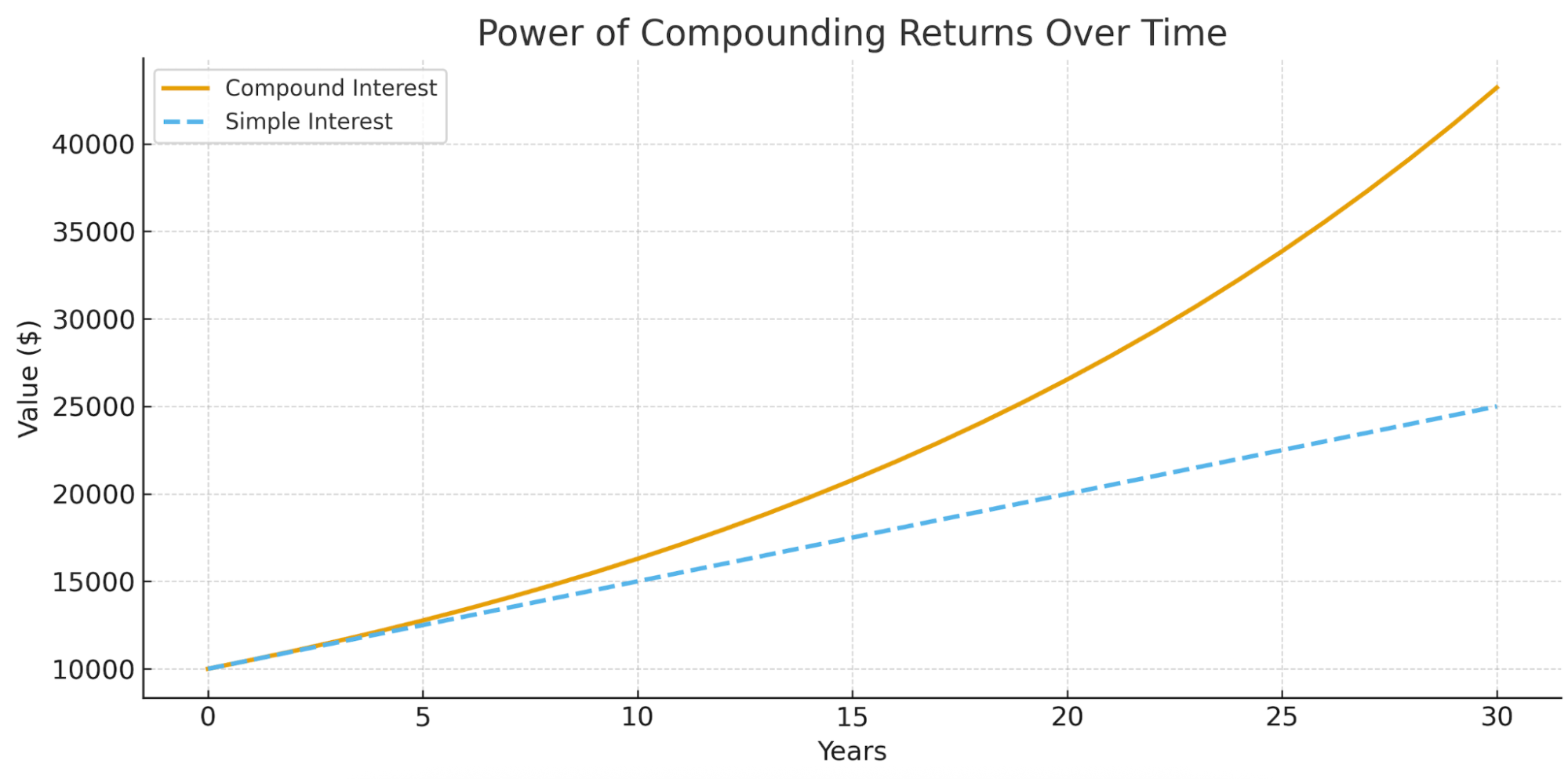

A £10,000 investment compounded at 5% annually will - by the law of mathematics - increase to more than £40,000 after 30 years. With the laws of mathematics offering a solid backdrop, the main job of investors is to find a high enough while also reliable return to let compounding do its work over time.

QUOTE

Money makes money. And the money that money makes, makes money.

Big ideas

- Compound interest can be thought of as interest on interest. Users earn interest on both the principal and the accumulated interest. This distinguishes it from simple interest, which applies only to the initial sum.

- Many of the world’s most successful investors have cited compound interest as a key element in their financial growth.

- Compound interest really shows its value in later years and applies to investors with multi-decade-long timelines. NOTE: It starts to really demonstrate its value over simple interest around year 15.

What is compound interest?

DEFINITION

Compound interest is interest that is added to the initial investment, but this addition increases future interest payments.

In this way, the more times the compounding takes place, the greater the future interest and overall payment.

In this way, the more times the compounding takes place, the greater the future interest and overall payment.

Chart showing 5% annual interest on an initial $10,000 investment.

Compound interest might be the eighth wonder of the world, but nobody knows where the original quote came from. At various times it has been attributed to Albert Einstein, J.D. Rockefeller, and Baron Rothschild, but without proof.

But whomever made that specific quote aside, Warren Buffett along numerous other wealthy investors have cited the power of compound interest in building wealth, on multiple occasions.

But whomever made that specific quote aside, Warren Buffett along numerous other wealthy investors have cited the power of compound interest in building wealth, on multiple occasions.

We know that Benjamin Franklin left £1,000 (~$5,000) to two US cities (Boston and Philadelphia) to be spent after 200 years, to actively demonstrate the power of compounding. The total was over $2 million for one city and $4.5 million for the other, released around 1991.

How does compound interest work?

Interest can be compounded at different intervals, typically annually, quarterly, or monthly. The more compounding periods there are, the greater the overall return. Different financial products will have different compounding periods.

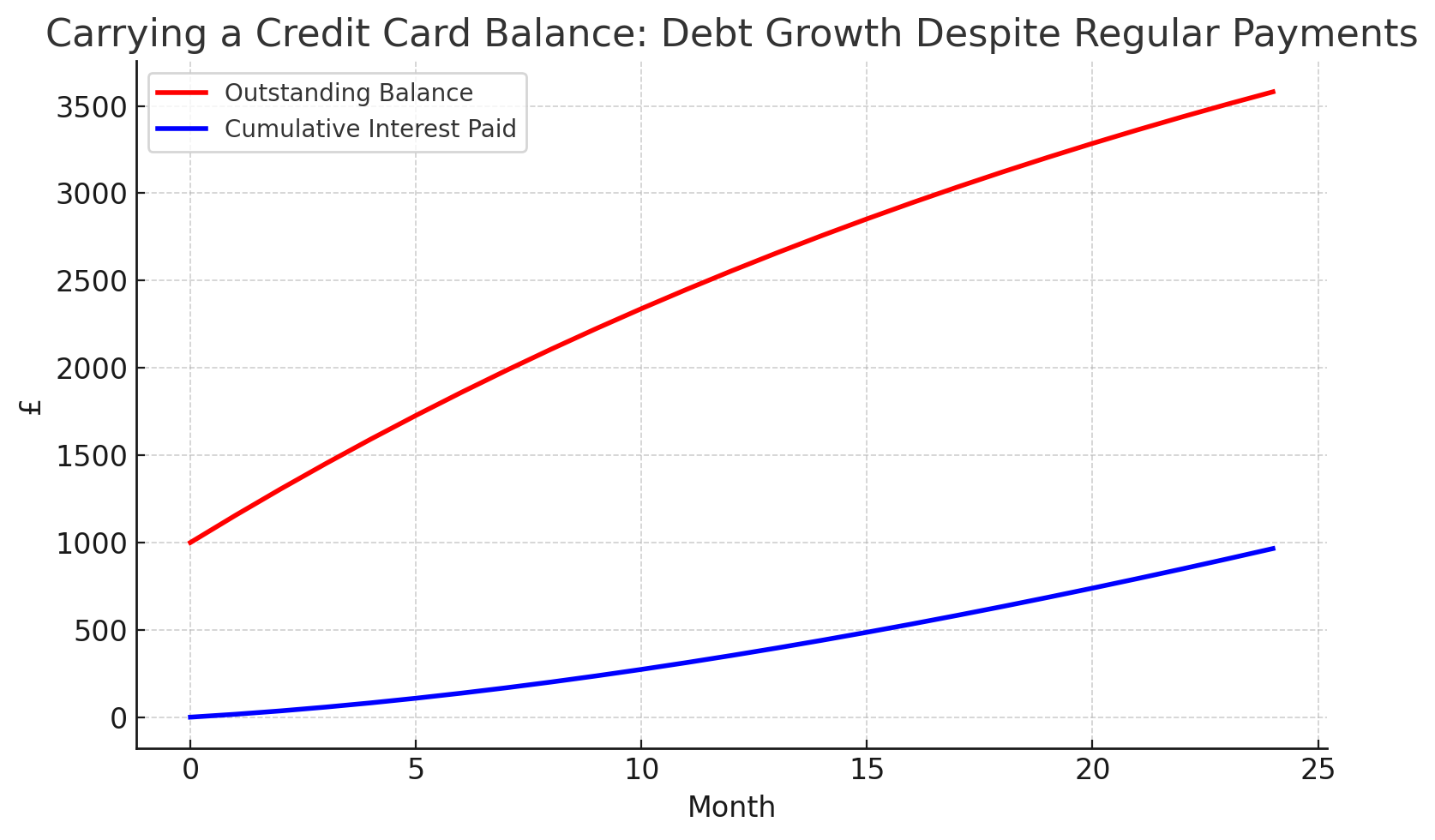

Consider also that compound interest can also work against you, in the case of debt. The same principle applies in the opposite fashion. You don’t want to go into a ‘debt’ spiral where you compound in the wrong direction, owing interest on top of interest. This is in effect what happens when you don’t pay off your credit card balance in full each month.

Consider also that compound interest can also work against you, in the case of debt. The same principle applies in the opposite fashion. You don’t want to go into a ‘debt’ spiral where you compound in the wrong direction, owing interest on top of interest. This is in effect what happens when you don’t pay off your credit card balance in full each month.

The above chart shows a simplified example of how adding £200 monthly spending while making only minimum 5% payments keeps debt rising. Interest compounds faster than payments reduce the balance, so the total owed and interest both climb steadily over time.

Why is compounding considered a wonder? Power of Compounding

Compound interest is considered a wonder because of its capability to passively increase returns incrementally through time with no effort on part of the investor. All that needs to be done is wait and observe.

So long as you can secure a compounding interest rate on a sum of money, the returns are predictable. Plus, the rewards are huge in proportion to the initial sum invested. A tiny amount can go a long way, thanks to the power of compounding.

The problem lies in first saving the money, and then finding the right saving account, money market account or other financial instrument to give you a good and secure rate, over a long time horizon. Compounding shows its value over the decades, so it’s important that the provider is financially stable, and that you have some kind of, possibly government-backed, insurance over your deposit.

So long as you can secure a compounding interest rate on a sum of money, the returns are predictable. Plus, the rewards are huge in proportion to the initial sum invested. A tiny amount can go a long way, thanks to the power of compounding.

The problem lies in first saving the money, and then finding the right saving account, money market account or other financial instrument to give you a good and secure rate, over a long time horizon. Compounding shows its value over the decades, so it’s important that the provider is financially stable, and that you have some kind of, possibly government-backed, insurance over your deposit.

What is the difference between simple and compound interest?

The difference between simple and compound interest is that simple interest is static and applies independently of previous interest.

FORMULA

Simple interest

SI = P × i × n

Where:

• SI = Simple Interest

• P = Principal (initial amount)

• I = Annual interest rate (in decimal form)

• n = Time period in years

SI = P × i × n

Where:

• SI = Simple Interest

• P = Principal (initial amount)

• I = Annual interest rate (in decimal form)

• n = Time period in years

EXAMPLE

A £10,000 principal at 5% yields £500 a year, every year, as long as the term lasts.

Compound interest is more complicated to calculate as previous interest rate payments are taken into account. This is what makes the end sum larger. It’s interest on interest, as opposed to interest on principal alone.

FORMULA

Compound interest

CI = P(1 + i)^n − P

Where:

• P = Principal

• i = Annual interest rate

• n = Number of compounding periods

CI = P(1 + i)^n − P

Where:

• P = Principal

• i = Annual interest rate

• n = Number of compounding periods

What would be the annual compound interest earned on £5,000 at 4% over ten years?

• P = £5,000

• i = 0.04 (4%)

• n = 10 years

Step 1: Add 1 to the rate: 1 + 0.04 = 1.04

Step 2: Raise to the power of years: 1.04¹º= 1.48

Step 3: Multiply by principal: 5,000 × 1.48 = 7,401.20

Step 4: Subtract the original amount: 7,401 − 5,000 = 2,401

Compound Interest earned: £2,401

Total amount after 10 years: £7,401

• P = £5,000

• i = 0.04 (4%)

• n = 10 years

Step 1: Add 1 to the rate: 1 + 0.04 = 1.04

Step 2: Raise to the power of years: 1.04¹º= 1.48

Step 3: Multiply by principal: 5,000 × 1.48 = 7,401.20

Step 4: Subtract the original amount: 7,401 − 5,000 = 2,401

Compound Interest earned: £2,401

Total amount after 10 years: £7,401

The Rule of 72 in investing

More commonly, investors will use the rule of 72 to check when their return will double. It’s very easy to calculate - all you need to do is to divide 72 by your interest rate.

If you have a 3% interest rate, it will take 24 years to double your initial principal. If you have a 4% interest rate, it will take 18 years, and if you have a 5% interest rate, it will take 14 years.

This also demonstrates that a mere 1% difference can result in an extra 6 years or more in terms of the time it takes to double a sum.

If you have a 3% interest rate, it will take 24 years to double your initial principal. If you have a 4% interest rate, it will take 18 years, and if you have a 5% interest rate, it will take 14 years.

This also demonstrates that a mere 1% difference can result in an extra 6 years or more in terms of the time it takes to double a sum.

How do I compound my money?

Compounding is a passive approach. After finding a financial provider offering a compound interest rate for deposits, you merely allow the funds to compound, with time.

It takes patience, and investors must be careful that they won’t need the funds for anything else. Remember, compounding works in terms of decades, not years, to see real returns.

Still, there are various forms of compounding, and different ways to apply it, including different frequency rates. Methods include the 7-3-2 and 8-4-3 approaches to compounding.

It takes patience, and investors must be careful that they won’t need the funds for anything else. Remember, compounding works in terms of decades, not years, to see real returns.

Still, there are various forms of compounding, and different ways to apply it, including different frequency rates. Methods include the 7-3-2 and 8-4-3 approaches to compounding.

What is the 7-3-2 rule of compounding?

The 7-3-2 rule is a way of thinking about the expanded benefits of compounding over time by setting financial goals to be achieved in a number of years.

The idea is that earning the first milestone takes 7 years but earning that same amount a second time only takes 3 years, then only 2 years the third time. Via the number of years it takes to earn a certain amount - you can visualise the increased effect of returns earning their own returns over time.

The idea is that earning the first milestone takes 7 years but earning that same amount a second time only takes 3 years, then only 2 years the third time. Via the number of years it takes to earn a certain amount - you can visualise the increased effect of returns earning their own returns over time.

What is the 8-4-3 rule of compounding?

The 8-4-3 rule of compounding is largely identical to the 7-3-2 rule, except it uses a different timeframe of 8, 4, and 3 years. The idea is the same, in that the results are seen in half the time, after the initial hurdle is passed

These rules should not be viewed as a definite set of results to be expected but rather concepts to help people understand roughly what returns are achievable as time passes.

These rules should not be viewed as a definite set of results to be expected but rather concepts to help people understand roughly what returns are achievable as time passes.

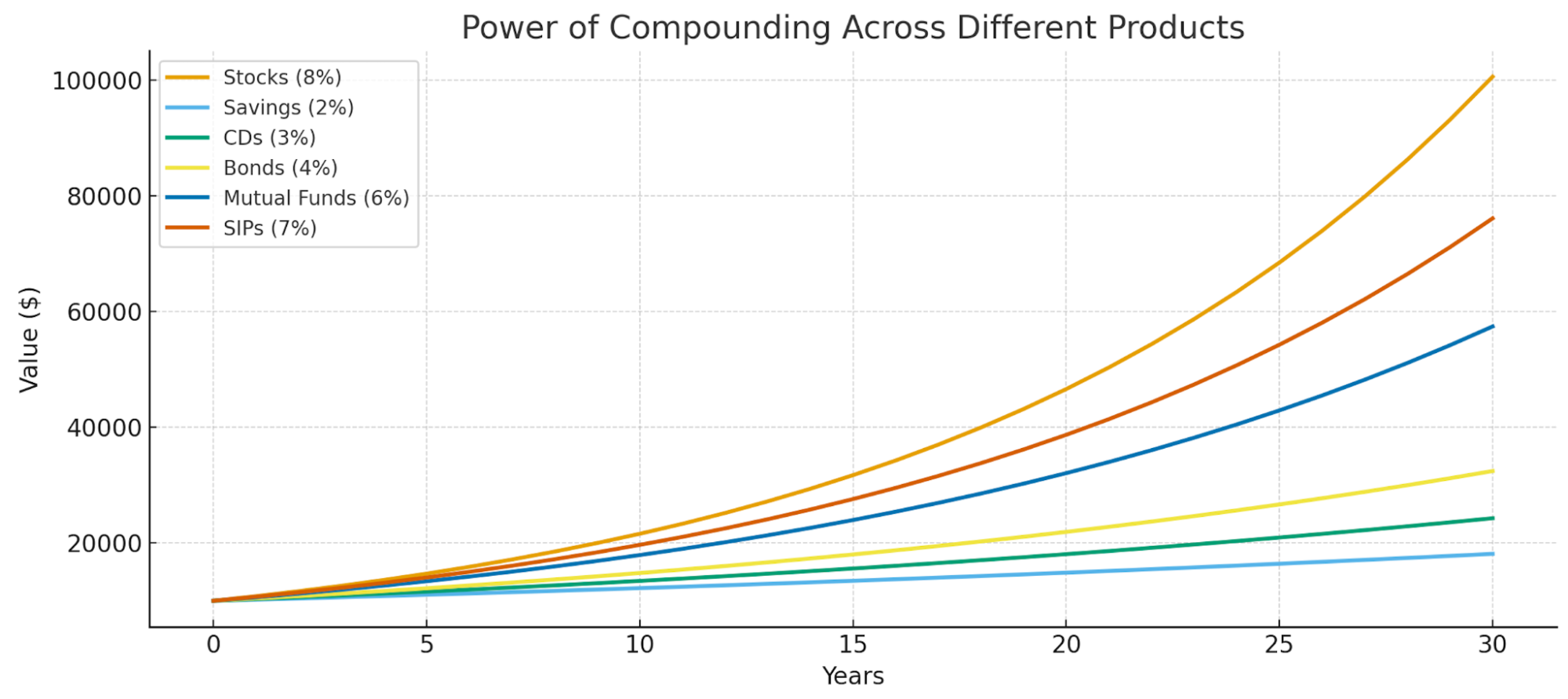

Compounding in different financial products

Compounding behaves differently depending on the financial product in question. The core premise remains the same, but you will get different intervals and rates. Stocks, for example, still offer the highest rates, and also the highest risk.

1. Stocks

When it comes to stocks, compounding happens through reinvested gains. If the stock price grows and dividends are put back into buying more shares, the base amount keeps increasing. Over time, each new share can also earn returns, building a snowball effect.

The higher expected returns are a result of the increased risk associated with owning shares, which by their nature can fall in value. While stock prices move up and down, the principle is that staying invested long enough via a diversified portfolio allows compounding to work quietly in the background.

The higher expected returns are a result of the increased risk associated with owning shares, which by their nature can fall in value. While stock prices move up and down, the principle is that staying invested long enough via a diversified portfolio allows compounding to work quietly in the background.

2. Savings accounts

In a savings account, interest compounds on the money deposited into the account. The bank adds a set interest amount at regular times, and then new interest grows on the bigger balance. It’s simple but steady growth, with lower risk. The rate might not be very high, but over time, the power of compounding can make even small deposits add up to something meaningful without much effort on the part of the saver.

3. Certificates of Deposits

With certificates of deposits (CDs), you lock in your money for a fixed time at a fixed rate. In the UK, a close equivalent is a fixed-rate savings account from your bank. Interest builds on the starting amount and then on the interest already earned. Since rates are guaranteed, the compounding can be easily predicted. It may not offer huge returns, but CDs give a higher return than savings accounts but likely a lower return over longer periods than stocks.

4. Bonds

Bonds pay interest through regular coupon payments. If that interest is reinvested into buying more bonds or similar products, compounding comes into play. Over the years, the growing interest payments can increase your overall investment. While bonds are generally more stable than stocks, the rate of return can vary depending on the bond type and issuer.

5. Mutual funds

Mutual funds can grow through both price gains and reinvested distributions. When interest, dividends, or capital gains are put back into the fund, the investment base gets larger. This means future gains apply to a bigger amount, which can build over time. Even small amounts can grow faster when left untouched for many years, as the compounding effect naturally multiplies returns without extra effort. While mutual funds can benefit from compounding over time, they are still exposed to market fluctuations and may experience periods of negative performance.

In what ways might investing and saving affect long-term wealth differently?

Saving and investing are not the same thing. With savings, money is tucked away in a bank account or a similar easy access, low ROI asset. This might be a money market instrument such as a certificate of deposit, where users might expect to earn something in the realm of 1% - 3%. This allows for low risk and maximum liquidity.

Investing is different, where funds are sent to higher risk assets like stocks, ETF, mutual fund, or corporate bonds. The expected returns should be from 5% - 10% or sometimes higher. But the asset can also decrease in value.

The core principle of life-cycle investing is to invest more aggressively in your earlier years then decrease your risk-taking in later years when you approach retirement.

Investing is different, where funds are sent to higher risk assets like stocks, ETF, mutual fund, or corporate bonds. The expected returns should be from 5% - 10% or sometimes higher. But the asset can also decrease in value.

The core principle of life-cycle investing is to invest more aggressively in your earlier years then decrease your risk-taking in later years when you approach retirement.

Recap

Compound interest is one of the most powerful financial tools available to investors looking to build long-term wealth. It’s reliable and mathematically precise.

The issue lies in human error and unexpected life events. It can be difficult to forgo consumption to save and invest a large sum of money and leave it untouched for ten years or more, especially when times are more uncertain. Remember though, even a small amount, can compound significantly over the decades, if left untouched.

When investing, your capital is at risk. Images for illustration purposes, not indicative of future performance.

The issue lies in human error and unexpected life events. It can be difficult to forgo consumption to save and invest a large sum of money and leave it untouched for ten years or more, especially when times are more uncertain. Remember though, even a small amount, can compound significantly over the decades, if left untouched.

When investing, your capital is at risk. Images for illustration purposes, not indicative of future performance.

FAQ

Q: What is compound interest in simple terms?

Compound interest is when the money you earn also starts to earn more money. Instead of getting interest only on your original amount, you get it on both the original and the added interest. Over time, this makes your savings or investments grow faster, like a snowball rolling and getting bigger.

Q: How do I calculate compound interest?

To find compound interest, use this formula: P (1 + i)^n − P, where P is the starting amount, i is the interest rate, and n is the number of years. This shows how much extra your money earns over time, as interest builds on top of itself each period.

Q: What does it mean to compound a debt?

Compounding a debt means the interest you owe is added to the total amount, and then new interest is charged on that bigger sum. This can make what you owe grow faster if not paid. It is the same idea as compounding savings, but it works against you instead of for you.

Q: What is the difference between compounding and discounting?

Compounding is about growing money over time, like building interest on top of interest. Discounting does the opposite. It works backward to find out what a future amount is worth today. Compounding moves money forward in time, while discounting moves it back, often used in pricing or valuing investments.

Q: What is a compounding interest savings account?

A compounding interest savings account is a bank account where your interest is added to your balance, and then future interest is earned on that bigger amount. It helps your savings grow faster than simple interest because the gains keep building over time. Many banks offer daily, monthly, or yearly compounding.

Q: What investments have compound interest?

Many investments can grow through compounding. Common examples include savings accounts, bonds, mutual funds, and dividend-paying stocks. Reinvesting earnings lets your money build on itself. Even small amounts can grow a lot over time, especially when left untouched, as compounding quietly increases the total balance year after year.